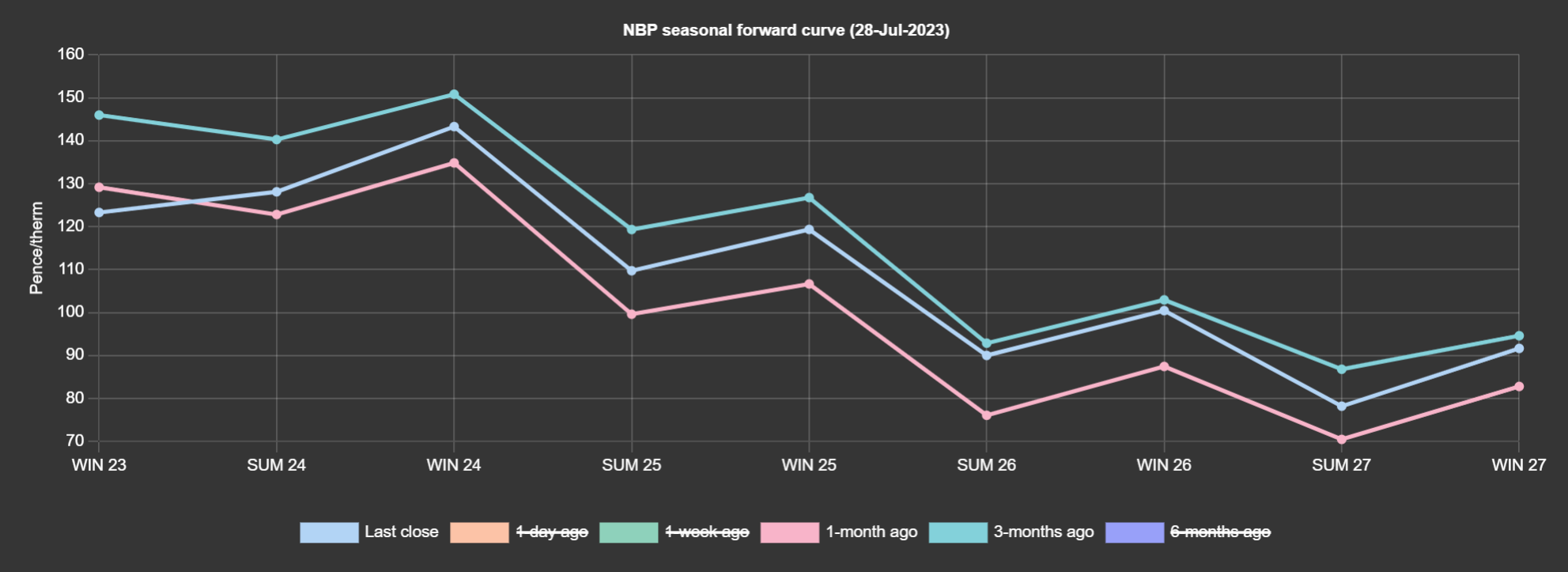

The week has ended on a bearish note, primarily due to increasingly benign supply/demand dynamics. In short, demand is low, supply is high, European storage is 15% above the 5-year average, high wind outputs forecast for August will mean lower gas-for-power generation. Whilst prices are up on the month, they remain down versus 3-months ago (see chart). The last few weeks has seen bullish price reactions to the high temperatures across Europe and Asia – however, this week we’ve seen a meaningful drop-off with below average seasonal temperatures forecast for central Europe into next week. Price action remains rangebound with psychological/impenetrable seasonal support levels at 106p/therm, and resistance at 140p/therm. At the time of writing, Winter ’23 delivery is toward the bottom of this trading bracket at 118p/therm. A break below 106p/therm for Winter’ 23 delivery remains very unlikely – as we approach the bottom of the range, any clients with Winter ’23 trades still to execute would surely be looking to transact before the onset of the shoulder month in 34 days’ time – after which, all eyes will be on long range weather forecasts and Asian bids for Winter ’23 LNG deliveries. Unweighted (Heren) monthly Day-Ahead averages are on target to achieve 72p/therm (or 2.4p/kwh). Outlook is neutral to bearish.

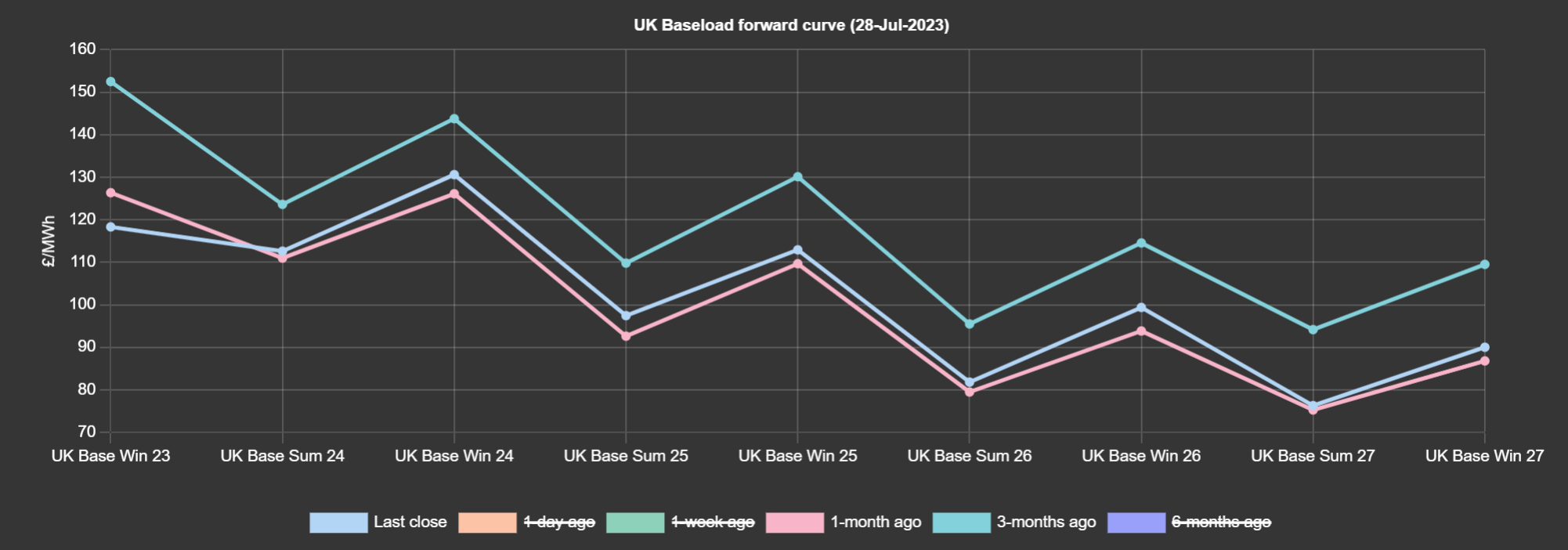

On the continent, short-term delivery prices are expected to fall next week, pressured by weaker demand, stronger renewables output and improving nuclear availability. Back in the UK, Winter ’23 delivery is down on the month AND versus 3-months ago (see chart). At the time of writing, Winter ’23 delivery is at £115/mwh with established seasonal support at £113/mwh (tested and rejected on both 7th June and 17th July), so there remains a small chance of retesting £100/mwh for Winter ’23 delivery (this level was last seen in Dec ’21!) Today’s generation mix is pretty neutral with fossil fuels (gas and coal) and renewables neck-and-neck at 37%; low carbon is at 16% (nuclear and imports). Unweighted (N2EX) monthly Day-Ahead averages are on target to achieve £72/mwh (or 7.2p/kwh). Outlook is neutral to bearish.